Retirement Is Broken

Franchising Is How You Take It Back

Nobody retires at 65 anymore. Here’s why owning a franchise — and knowing how to fund it — changes everything.

Nobody retires at 65 anymore. Here’s why owning a franchise — and knowing how to fund it — changes everything.

Something strange is happening in today’s workforce. Some professionals race to leave the traditional grind by their mid-30s. Others, in their 70s and 80s, keep working — and not always by choice. The old promise of retiring at 65 with a pension? For most people, that story is over.

If you’re somewhere in between — watching your savings lag, your job security fade, and your choices shrink — these shifts are already yours to navigate. The good news: there’s a third path, and it’s more fundable than most people realize.

The Numbers Tell a Sobering Story

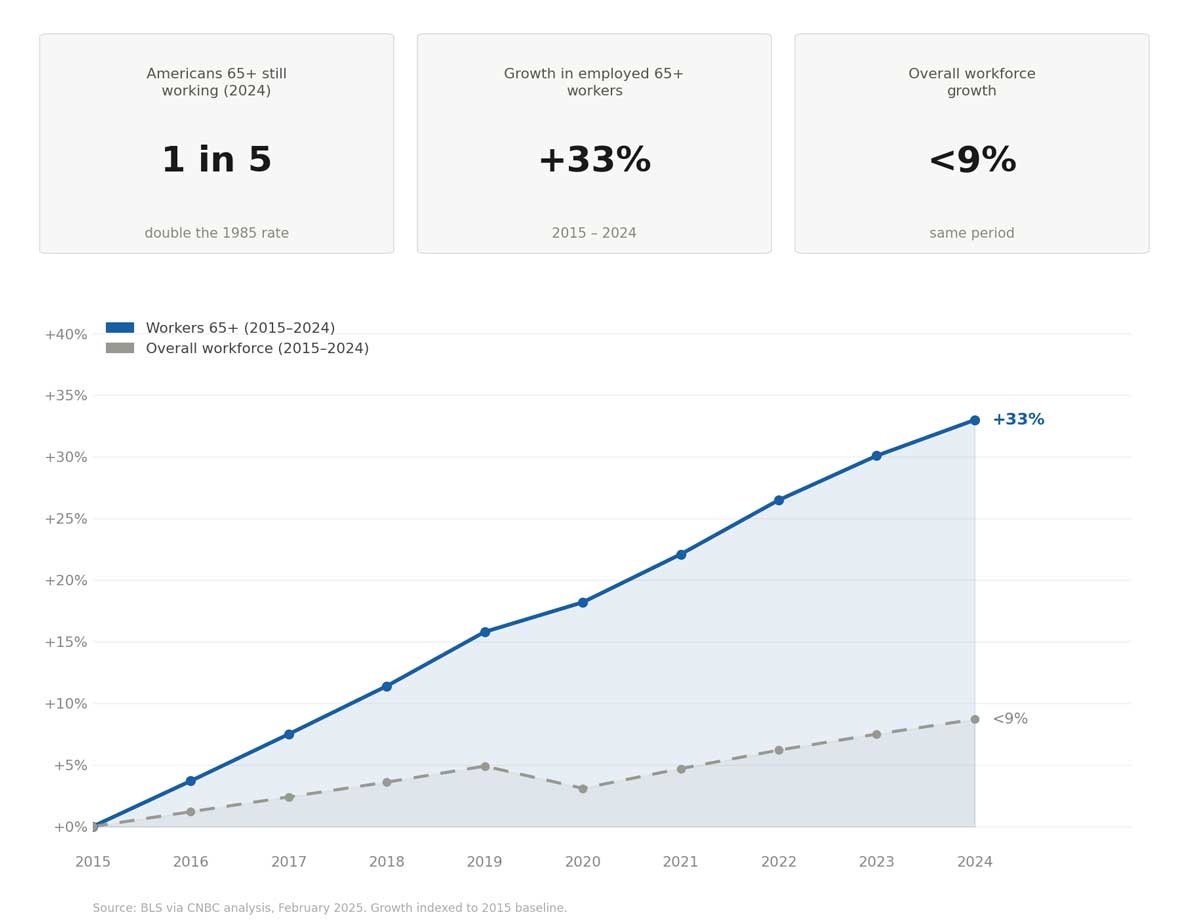

The U.S. Bureau of Labor Statistics reports that nearly one in five Americans aged 65 and older was still working as of 2024 — double the rate seen in 1985. Between 2015 and 2024, the number of employed Americans 65 and older grew by more than 33%, far outpacing the workforce’s overall growth of under 9% (CNBC analysis of BLS data, February 2025). The 75-and-older group is now the fastest-growing segment of the labor market.

Why? Rarely because people love Monday mornings. A February 2026 report from the National Institute on Retirement Security put the median retirement savings of working Americans at just $955. Even among those aged 55 to 64, the median sits around $185,000 — well below the $1.46 million Americans now say they’d need to retire comfortably (Northwestern Mutual, 2026).

Meanwhile, the FIRE movement (Financial Independence, Retire Early) keeps gaining ground. A Harris Poll survey of more than 2,000 people found that a quarter of Americans want to retire before age 50. The ones who pull it off share one trait: they stopped relying on a single paycheck and built income, equity, and ownership of their own.

The Middle Ground Has Disappeared

The person still working at 85 and the person who retired at 35 look like opposites. But they share the same disillusionment with one broken promise: work hard, save a little, retire at 65, and enjoy the rest. AI, economic uncertainty, and a shifting labor market have shattered it.

The person still working at 85 and the person who retired at 35 look like opposites. But they share the same disillusionment with one broken promise: work hard, save a little, retire at 65, and enjoy the rest. AI, economic uncertainty, and a shifting labor market have shattered it.

Here’s what today’s market actually looks like:

- U.S. job openings fell to 6.9 million in February 2026, and gross hires dropped to 4.85 million — the fewest since April 2020 (BLS JOLTS Report, March 2026).

- Voluntary quits hit their lowest point since August 2020 — a sign workers have lost confidence they can find something better.

- Economists call it a “low-hire, low-fire” market: few big layoffs, but few new openings either — meaning longer searches and little leverage for raises.

- Nearly 60% of jobs in advanced economies now have meaningful exposure to AI, which is rapidly absorbing routine work in coding, marketing, finance, and admin (International Monetary Fund).

Add ageism — longer searches and quiet screening-out for workers over 50, against an average U.S. unemployment spell of 22.9 weeks — and you get the modern trap: job-hugging. People cling to roles they’ve outgrown because the alternative feels worse.

Here’s the part nobody says out loud: in traditional employment, you’re not building equity. You’re trading time for money on someone else’s terms — and when those terms change, you start over from scratch.

Why Franchising Is the Answer

The people who retire early and the people who happily work past 65 actually share something: they stopped treating work as just a paycheck and started building the four pillars of Career Ownership — Income, Lifestyle, Wealth, and Equity.

A franchise is one of the most direct ways to build all four — because it lets you own a business without starting from zero. Instead of inventing a concept, you step into a proven model with an established brand, a documented playbook, training, and ongoing support. Your decades of experience become an asset rather than a liability, and the value you create is yours — an asset you own, not a position you rent.

Franchising won’t make the risk disappear, but it replaces the blank page with a tested system — which is exactly why so many career-changers in their 40s, 50s, and 60s choose it as their next chapter.

How to Fund a Franchise Today

One of the biggest myths about franchise ownership is that you need all the cash up front. You don’t. Most owners combine two or three sources. Here are the main ways people fund a franchise right now:

One of the biggest myths about franchise ownership is that you need all the cash up front. You don’t. Most owners combine two or three sources. Here are the main ways people fund a franchise right now:

- Personal savings & home equity. Cash on hand, plus a home equity loan or HELOC, is often the simplest starting point — frequently paired with one of the options below.

- SBA loans (7(a) and 504). Government-backed loans are among the most popular franchise-funding tools. A 7(a) can bundle the franchise fee, equipment, and working capital into one package with relatively low down payments; the 504 is geared toward real estate and large equipment. Many brands appear on the SBA’s franchise directory, which can streamline approval.

- 401(k)/IRA rollover (ROBS). A Rollover for Business Startups lets you use eligible retirement funds to buy a franchise without early-withdrawal penalties or taxes — and with no loan or monthly payments. It works by forming a C-corporation that sponsors a retirement plan, which then buys stock in your company. It’s powerful but complex, with setup costs and ongoing compliance, and your retirement savings are at stake — so it’s worth professional guidance.

- Conventional bank & credit-union loans. Traditional term loans offer predictable repayment if you have strong credit and collateral.

- Franchisor financing & preferred lenders. Many brands offer in-house financing or vetted lender programs (look in Item 10 of the Franchise Disclosure Document). The lender already understands the model, which can speed approval — just compare the terms.

- Business lines of credit & equipment financing. Flexible options for covering equipment, technology, build-out, and day-to-day working capital.

- Partners, investors & crowdfunding. Bringing in a partner or raising equity can cover the gap — in exchange for shared ownership.

- Veteran incentives (VetFran). If you’ve served, many franchisors offer reduced fees or special financing through programs like VetFran.

Terms, rates, and eligibility vary, and this isn’t financial advice — the right mix depends on your savings, credit, timeline, and goals. That’s exactly what the Funding Options Assessment is built to sort out: a quick, no-pressure way to see which funding paths realistically fit your situation — so “how would I ever pay for it?” turns into “here’s how I actually could.”

How a Career Ownership Coach® Closes the Gap

A Career Ownership Coach® isn’t a recruiter. They won’t polish your résumé or find you another job that could vanish in the next round of cuts. They’re a guide — someone who helps you see the full picture of what’s possible and what’s right for you, including how the numbers and the funding could actually work.

A Career Ownership Coach® isn’t a recruiter. They won’t polish your résumé or find you another job that could vanish in the next round of cuts. They’re a guide — someone who helps you see the full picture of what’s possible and what’s right for you, including how the numbers and the funding could actually work.

Together, you build a “career firewall” that protects what matters most — whether that’s strengthening your corporate strategy, layering in new income streams, or stepping into franchise ownership. Every conversation begins with the same question: what’s next for you?

Most people spend more time planning a two-week vacation than the next 20 years of their working life. A coach changes that, bringing clarity and structure to a decision that’s far too important to leave to chance.

The Real Retirement Plan

Retirement at 65 was always someone else’s benchmark — built for a world of pensions, predictable careers, and stable employers. That world is gone. The real goal isn’t to save a little more or work a little longer; it’s to start building Career Ownership now, so you control your income, your lifestyle, and the equity that’s genuinely yours.

Whether you’re 30 and done with the corporate grind or 55 and wondering what comes next, the path forward starts with one conversation — and a clear-eyed look at how to pay for it.

Take the Funding Options Assessment to discover the funding paths that could work for you — then connect with a Career Ownership Coach® through Franchise Match. The first conversation is on us, and it might be the most valuable one you have all year.